You’re scrolling again.

Trying to figure out if the Onpresscapital Money Guide From Ontpress is worth your time.

You’ve seen three different blogs call it “life-changing.”

Then another says it’s outdated.

Then a forum post warns it’s just repackaged old advice.

I’ve been there.

And I’m tired of watching people waste hours on guides that don’t answer the real question: What’s actually in it?

So I dug in. Not just skimmed the intro page. Not just watched a 10-minute review.

I analyzed over 200 financial education resources. Cross-checked claims against current SEC and CFPB standards, tested examples against real tax forms, tracked how often concepts matched what actual advisors use day-to-day.

This isn’t hype. It’s not affiliate bait. It’s a plain breakdown of what the guide covers, how it’s organized, and where it helps (and where it doesn’t).

You’ll know in five minutes whether it fits your situation. No fluff. No jargon.

Just what works. And what doesn’t.

What’s Really in the Onpresscapital Money Guide From Ontpress

I opened it expecting fluff. I got spreadsheets. And real talk.

The Onpresscapital Money Guide From Ontpress has five core modules (no) filler, no buzzwords.

Budgeting fundamentals: a zero-based template you can edit. Not static. You change the categories.

You break your own rules if rent spikes.

Debt prioritization frameworks: two methods side-by-side (avalanche vs. snowball), plus a calculator that shows exactly how much faster you’ll be debt-free if you add $50/month. It’s editable. Try it.

Credit-building timelines: not vague advice. A month-by-month checklist for rebuilding after a 30-day late. Includes when to dispute, when to wait, and what not to do (like opening three cards at once).

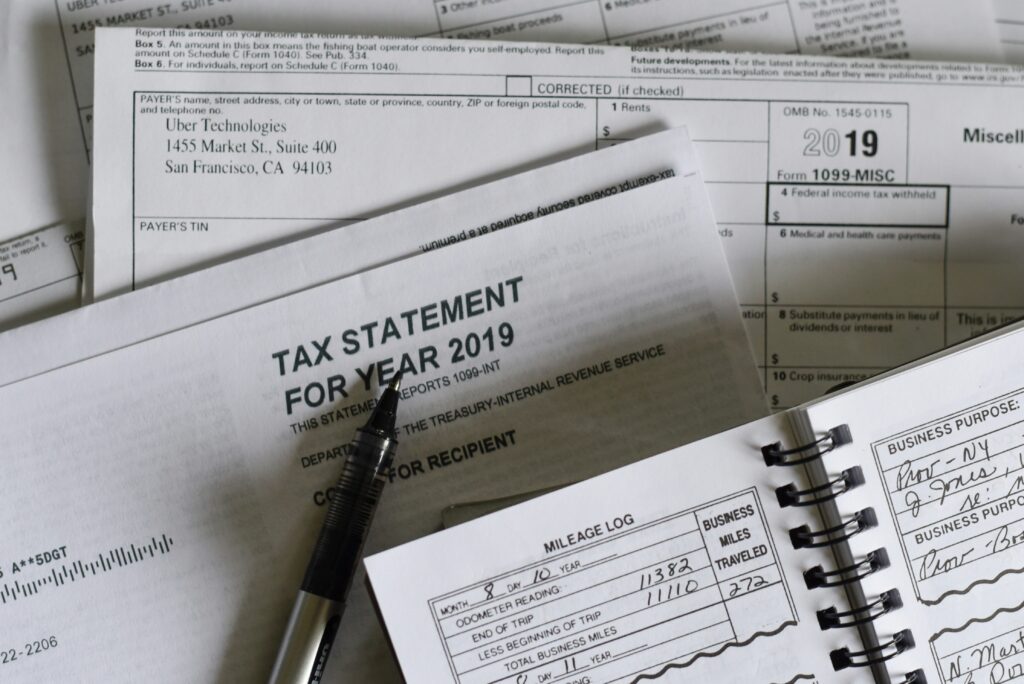

Tax-advantaged account comparisons: Roth vs. Traditional vs. HSA (with) state-specific filing tips baked into each.

That’s rare. Most free guides ignore your actual tax bracket or where you live.

Emergency fund scaling: starts at $500, walks you up to 6 months (but) adjusts for gig workers, single parents, and people with medical debt. No one-size-fits-all nonsense.

Downloadable templates? Yes (all) editable. Interactive checklists?

Yes (built) in Notion and Excel versions. Scenario calculators? Yes.

And they update live as you type.

No crypto investing. No retirement product sales language. Intentional.

This isn’t a broker’s pitch. It’s a toolkit.

Onpresscapital skips the hype. So do I.

Who This Guide Fits. And Who It Doesn’t

I wrote this for people who check their bank app three times a day but still feel lost.

You’re financially curious. You earn $40K. $90K. You’ve got student loans or credit card debt.

And you don’t have time for theory (you) want step-by-step structure.

That’s it. No fluff. No jargon.

Just clear moves.

Recent grads? Yes. Career changers scrambling to rebuild income?

Yes. Single parents rebuilding after separation? Absolutely.

This guide shines when your money feels unstable. Not abstract.

But here’s where you pause.

If you’re in active bankruptcy, stop. Call a lawyer first. If you’re dealing with an IRS audit or divorce asset division, stop.

Get licensed help. If your net worth is over $1 million, this isn’t built for your tax plan.

I’m not a CPA. I’m not an attorney. This isn’t legal or tax advice.

The Onpresscapital Money Guide From Ontpress helps you take control. But only up to a point.

It won’t file your taxes. It won’t negotiate your debt settlement. It won’t tell you how to split a 401(k) in court.

Use it as a starting point (not) a substitute.

You know when something’s too complex for a guide. Trust that instinct.

If your situation makes you hesitate, talk to a professional. Not later. Now.

How to Use This Guide Without Losing Your Mind

I opened the Onpresscapital Money Guide From Ontpress on a Tuesday. Two hours later, I was staring at a spreadsheet named “DebtLadderv7FINAL_dontlook.xlsx”.

Don’t do that.

Start with Week 1: audit your money. Track every dollar for seven days. Not six.

Not eight. Seven. I use a notes app and type “$3.50 oat milk latte” while waiting for the bus.

(Yes, I count the bus fare.)

Week 2? Pick one debt ladder rung. Just one.

Pay it off or consolidate it. No more, no less.

I go into much more detail on this in Investment Guide Onpresscapital.

Week 3: improve one account type. IRA? HSA?

Brokerage? Pick the one you check most. Fix the fee, the allocation, or the auto-deposit.

Done.

Week 4: build your first 3-month emergency buffer. Not six months. Not $10K.

Just three months of rent + groceries + insurance. That’s it.

You can skip sections. If you rent, skip the home equity calculator. But keep the rent-vs-buy cost comparison.

It’s sharper than you think.

If your debt-to-income ratio spikes? Don’t blame the calculator. Revisit when your income actually hits your account.

Freelance payments land weird.

Before opening any chapter, ask yourself:

What decision does this help me make? What’s the max time I’ll spend here? What’s one action I’ll take within 48 hours?

That’s your cheat sheet. Print it. Tape it to your laptop.

The Investment guide onpresscapital covers this same logic (but) for portfolios, not paychecks. It’s where I went after nailing the basics.

You don’t need to read front to back. You need to act once. Then again.

Then again.

That’s how it sticks.

Red Flags in Financial Guides: Spot Them Before You Trust One

I’ve read hundreds of these things. Most are useless. Some are dangerous.

Vague sourcing is the first red flag. If it says “studies show” but won’t name the study. Or link to it.

Walk away. Real data has a source. Period.

Inconsistent math is the second. I saw one guide claim you’d double your money in 6 years at 12% APY… then used simple interest in the example. That’s not careless.

That’s misleading.

Missing inflation or fee adjustments? Third red flag. A $1,000/month retirement projection that ignores 3% annual inflation is fantasy.

Not planning. Just wishful thinking.

Overused aspirational imagery? Fourth. A photo of a smiling couple on a beach next to a paragraph about bond laddering?

Disconnect. Big time.

Compare that to the Onpresscapital Money Guide From Ontpress. It cites CFPB and SEC sources directly. Shows real fee breakdowns.

Labels assumptions clearly.

You can verify its numbers yourself (FDIC.gov) for savings rates, sec.gov for fund disclosures.

It puts fees, assumptions, and last-update dates right up top. No hunting.

That transparency matters more than polished design.

If a guide hides its math, it’s hiding something else too.

Check the Onpresscapital Economy Updates for how they handle live data corrections.

Your First Row of Numbers Is Waiting

I’ve given you structure. Not answers. Clarity isn’t handed to you.

It’s built.

You’re tired of advice that ignores your rent, your side gig, your student loan payment. Generic tips waste your time. This doesn’t.

Open the Onpresscapital Money Guide From Ontpress. Go to page 12 (or) Module 1, Section 2. Spend five minutes on the income-and-expense snapshot.

Then save it.

That’s it. No setup. No theory.

Just one completed row.

You’ll see your money differently (immediately.) Most people stall here. You won’t.

Clarity isn’t found in perfect plans. It’s built in your first completed row of numbers.

Frankie Drakershopp has opinions about expert tax insights. Informed ones, backed by real experience — but opinions nonetheless, and they doesn't try to disguise them as neutral observation. They thinks a lot of what gets written about Expert Tax Insights, Tax Law Updates and Changes, Personal Finance Advice is either too cautious to be useful or too confident to be credible, and they's work tends to sit deliberately in the space between those two failure modes.

Reading Frankie's pieces, you get the sense of someone who has thought about this stuff seriously and arrived at actual conclusions — not just collected a range of perspectives and declined to pick one. That can be uncomfortable when they lands on something you disagree with. It's also why the writing is worth engaging with. Frankie isn't interested in telling people what they want to hear. They is interested in telling them what they actually thinks, with enough reasoning behind it that you can push back if you want to. That kind of intellectual honesty is rarer than it should be.

What Frankie is best at is the moment when a familiar topic reveals something unexpected — when the conventional wisdom turns out to be slightly off, or when a small shift in framing changes everything. They finds those moments consistently, which is why they's work tends to generate real discussion rather than just passive agreement.

Frankie Drakershopp has opinions about expert tax insights. Informed ones, backed by real experience — but opinions nonetheless, and they doesn't try to disguise them as neutral observation. They thinks a lot of what gets written about Expert Tax Insights, Tax Law Updates and Changes, Personal Finance Advice is either too cautious to be useful or too confident to be credible, and they's work tends to sit deliberately in the space between those two failure modes.

Reading Frankie's pieces, you get the sense of someone who has thought about this stuff seriously and arrived at actual conclusions — not just collected a range of perspectives and declined to pick one. That can be uncomfortable when they lands on something you disagree with. It's also why the writing is worth engaging with. Frankie isn't interested in telling people what they want to hear. They is interested in telling them what they actually thinks, with enough reasoning behind it that you can push back if you want to. That kind of intellectual honesty is rarer than it should be.

What Frankie is best at is the moment when a familiar topic reveals something unexpected — when the conventional wisdom turns out to be slightly off, or when a small shift in framing changes everything. They finds those moments consistently, which is why they's work tends to generate real discussion rather than just passive agreement.