What Education Tax Credits Are (And Why They Matter in 2026)

Education tax credits are one of the rare opportunities in the tax code that directly shrink what you owe dollar for dollar. Unlike deductions, which lower your taxable income, credits apply to your actual tax bill. If you’re eligible for a $2,000 credit, that’s $2,000 off your tax due. Simple math, strong impact.

Qualifying isn’t just about being a student. The credits can apply to undergrads, grad students, part time learners even the parents or spouses footing the bill. The catch: the student must be enrolled in an eligible school, and the taxpayer claiming the credit must meet income requirements.

As we head toward 2026, staying updated is crucial. The IRS regularly tweaks thresholds, definitions, and required documentation. A missed update say, a new income phase out limit could mean leaving money on the table. With the pace of changes picking up, informed filers will win.

If you’re paying for school or supporting someone who is, education tax credits deserve your attention. They’re not just a financial perk they’re a strategic move on your tax return.

The Two Main Education Tax Credits

When it comes to reducing the cost of higher education, two major federal credits can significantly lower your tax bill. Here’s a breakdown of what each offers and how to determine which one fits your situation best.

American Opportunity Tax Credit (AOTC)

The AOTC is designed to support undergraduate students and the families footing the bill for college. It offers a substantial opportunity to reduce taxes, and even receive money back if your tax liability is zero.

Key Highlights:

Educational Stage: Only available for the first four years of postsecondary education.

Maximum Credit: Earn up to $2,500 per eligible student each year.

Refundable Portion: 40% of the credit is refundable, meaning you can receive up to $1,000 even if you owe no taxes.

Eligibility Checklist:

Student must be enrolled at least half time in a degree, certificate, or recognized credential program.

Taxpayer’s modified adjusted gross income (MAGI) must fall within IRS limits.

You must receive a Form 1098 T from an eligible educational institution.

Good to Know:

Expenses must be for tuition, required fees, and qualified course materials.

The credit is per student, not just per tax return.

Lifetime Learning Credit (LLC)

The LLC offers more flexibility than the AOTC and is better suited for a wider range of learners, including nontraditional students and those pursuing ongoing education.

Key Highlights:

Educational Stage: Available for any postsecondary education or professional development, with no limit to the number of years claimed.

Maximum Credit: Provides up to $2,000 per tax return, regardless of how many students are claimed.

Nonrefundable: The LLC can reduce your tax bill to zero, but won’t provide money back if no tax is owed.

Ideal For:

Part time students

Graduate program enrollees

Adults seeking new skills or credentials

Flexibility:

You don’t need to be enrolled in a degree program.

Expenses can include tuition and fees related to career advancement, certification, or new skills acquisition.

Caveat:

Only one credit (either AOTC or LLC) can be claimed per student in a given tax year.

Both credits offer powerful ways to reduce college expenses you just need to know which one aligns with your goals and circumstances.

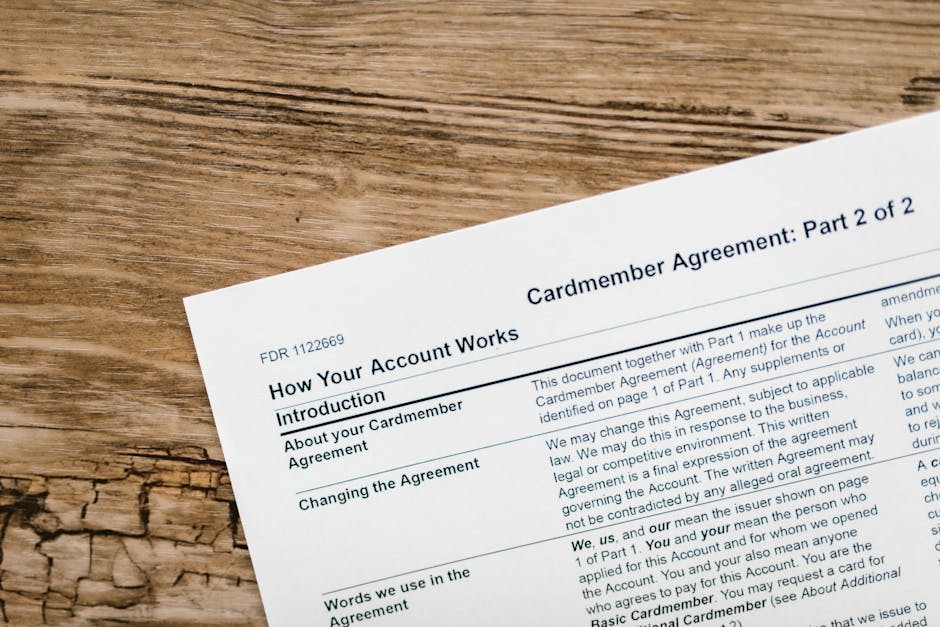

To claim an education tax credit in 2026, you’ll need to start with IRS Form 1098 T the Tuition Statement. Your school is required to send it to you by January 31st. Don’t ignore it. This document shows the amount billed or paid for qualified tuition and related expenses, which is key to calculating your credit.

Next, you’ll need to complete IRS Form 8863. This is where the real action happens. It’s where you’ll figure out whether you qualify for the American Opportunity Tax Credit (AOTC), the Lifetime Learning Credit (LLC), or neither and plug in the numbers from your Form 1098 T.

Pro tip: double check your eligibility details before filing. Tax benefits depend on everything from your income to your residency to whether someone else is claiming you as a dependent. One mistake here can kill your credit or delay your refund.

And here’s a rule that trips people up every year: you can’t claim both credits for the same student in the same tax year. You have to pick one whichever gives you the best value based on your situation.

Get your paperwork right, choose wisely, and don’t leave money on the table. These credits can be serious financial relief if you play it smart.

Choosing between education tax credits and deductions isn’t just paperwork it can change your refund or final bill by hundreds, sometimes thousands. Get it wrong, and you leave money on the table. The key? Credits usually deliver more bang for your buck. Deductions reduce taxable income. Credits cut straight into the amount you owe, dollar for dollar. So if you qualify for a credit, especially refundable ones like the American Opportunity Tax Credit (AOTC), take it.

But don’t stop there. Keep an eye on phase out income limits these change annually and can quietly edge you out of eligibility. If your adjusted gross income gets too high, a credit you counted on might vanish. That’s a nasty surprise come April.

And if you’re self employed or juggling multiple write offs (side hustle, part time studies, etc.), make sure everything lines up clean. A mismatch between tuition claims and home office deductions can trigger flags. For extra help navigating overlapping benefits, especially if you’re filing solo, check out A Guide to Home Office Tax Deductions for Self Employed Filers. Smart tax planning isn’t just about saving it’s about steering clear of mistakes you can’t afford.

Maximize Your Credit Value

Getting the full benefit from education tax credits takes more than just filling out the right form. It starts with tracking your expenses like it matters because it does. Keep every tuition and fee statement handy throughout the year. That includes Form 1098 T, receipts from your college bookstore, and invoices for course specific software or supplies. If it was required for coursework, it could count.

Don’t stop at tuition. The IRS allows for several qualifying expenses beyond tuition books, lab equipment, and even software can be eligible. A lot of people miss these and leave money on the table. Be methodical.

One strategic move? If you’re paying spring semester tuition in December, you may be able to apply it to the current year’s tax credit. This front loading approach can push your qualified expenses high enough to max out your benefit. Just be sure payments post before the calendar year ends. Timing matters.

A little planning and discipline here can make hundreds sometimes thousands in savings. Don’t wing it.

Staying Smart with Tax Benefits

The tax code doesn’t sit still. It changes every year, and that means staying lazy about it can cost you. January is the time to review updates new rules, adjusted phase out ranges, modified credit values. IRS revisions aren’t flashy, but they can quietly shift what you qualify for, and how much you get back.

Don’t go it alone if you don’t have to. Investing in solid tax software or speaking with a qualified advisor usually pays for itself. These tools catch things you might miss especially around education credits that come with nuance and fine print.

And here’s a common myth: if you don’t itemize, you’re out of luck. Not true. Education tax credits like the AOTC and LLC apply to your return regardless of whether you itemize deductions. They’re credits straight cuts off your tax bill, not vague subtractions in the background. Understand them, claim them, and use them to lower your liability where it counts.

Thadrian Xenvale is the kind of writer who genuinely cannot publish something without checking it twice. Maybe three times. They came to tax tips and strategies through years of hands-on work rather than theory, which means the things they writes about — Tax Tips and Strategies, Tax Deductions and Credits, Financial Planning for Taxes, among other areas — are things they has actually tested, questioned, and revised opinions on more than once.

That shows in the work. Thadrian's pieces tend to go a level deeper than most. Not in a way that becomes unreadable, but in a way that makes you realize you'd been missing something important. They has a habit of finding the detail that everybody else glosses over and making it the center of the story — which sounds simple, but takes a rare combination of curiosity and patience to pull off consistently. The writing never feels rushed. It feels like someone who sat with the subject long enough to actually understand it.

Outside of specific topics, what Thadrian cares about most is whether the reader walks away with something useful. Not impressed. Not entertained. Useful. That's a harder bar to clear than it sounds, and they clears it more often than not — which is why readers tend to remember Thadrian's articles long after they've forgotten the headline.

Thadrian Xenvale is the kind of writer who genuinely cannot publish something without checking it twice. Maybe three times. They came to tax tips and strategies through years of hands-on work rather than theory, which means the things they writes about — Tax Tips and Strategies, Tax Deductions and Credits, Financial Planning for Taxes, among other areas — are things they has actually tested, questioned, and revised opinions on more than once.

That shows in the work. Thadrian's pieces tend to go a level deeper than most. Not in a way that becomes unreadable, but in a way that makes you realize you'd been missing something important. They has a habit of finding the detail that everybody else glosses over and making it the center of the story — which sounds simple, but takes a rare combination of curiosity and patience to pull off consistently. The writing never feels rushed. It feels like someone who sat with the subject long enough to actually understand it.

Outside of specific topics, what Thadrian cares about most is whether the reader walks away with something useful. Not impressed. Not entertained. Useful. That's a harder bar to clear than it sounds, and they clears it more often than not — which is why readers tend to remember Thadrian's articles long after they've forgotten the headline.