I’ve helped thousands of small business owners figure out their taxes over the years.

You’re probably here because tax season is coming and you’re not sure where to start. Or maybe you just want to stop overpaying the IRS.

Here’s the truth: calculating your small business taxes isn’t as complicated as it seems. But most entrepreneurs make mistakes because they don’t have a clear process to follow.

I’m going to show you how to calculate taxes in a way that makes sense. No accounting degree required.

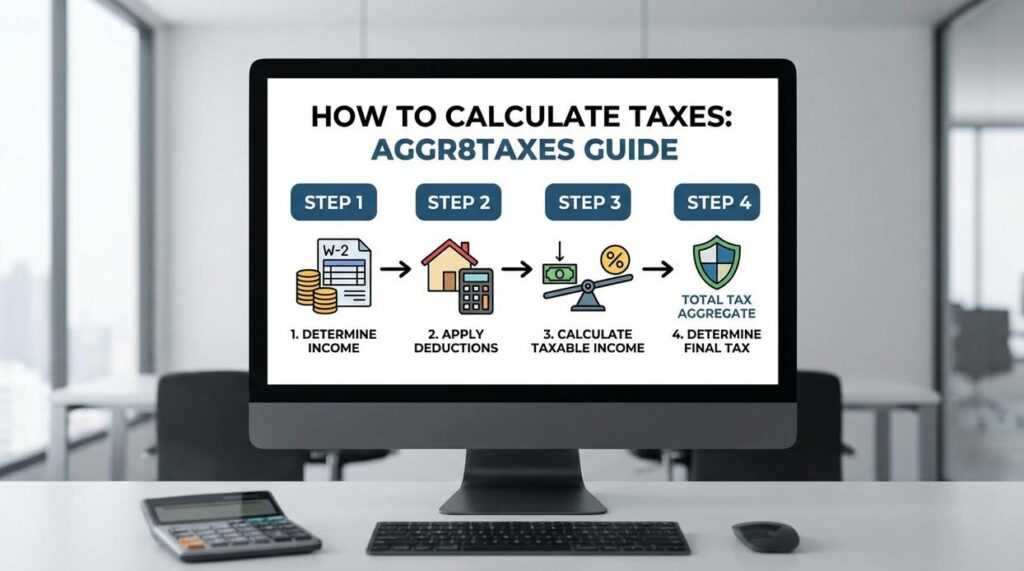

This guide walks you through the exact steps. You’ll learn how to gather the right documents, identify your deductions, and figure out what you actually owe in federal income and self-employment taxes.

I’ve spent years working with business owners who were overwhelmed by tax calculations. The ones who succeeded didn’t have some secret knowledge. They just followed a system.

You’ll get that system here. Each step is broken down so you can work through it at your own pace.

By the end, you’ll know your tax liability and feel confident you did it right.

No guesswork. No panic. Just a clear path from start to finish.

Step 1: Gather Your Essential Financial Documents

Look, I’m going to be blunt here.

If your records are a mess, your tax calculation will be a mess. There’s no way around it.

I’ve seen too many people try to piece together their taxes from memory or random receipts stuffed in a shoebox. It never ends well. You either overpay because you forgot deductions or you underpay and deal with the IRS later.

Neither option is fun.

Here’s what you actually need before you start to how to calculate taxes aggr8taxes.

Income records come first. Pull together your invoices, 1099-NEC forms, 1099-K forms, sales records, and bank deposit slips. Every dollar that came in needs documentation.

Expense records are next. Receipts, bank statements, credit card statements, mileage logs if you drove for work, and payroll records if you have employees. This is where most people leave money on the table (because they didn’t keep track).

Don’t forget asset information. If you bought or sold business property or equipment this year, you need those records. Depreciation matters more than you think.

And grab last year’s tax return. You might have losses or credits that carry forward. Missing these is like leaving cash sitting on the table.

Now, some tax pros will tell you that keeping every single receipt is overkill. They say the IRS doesn’t care about small expenses.

Maybe that’s true for a $3 coffee. But when audit season hits? You’ll wish you had everything documented.

The truth is this. Good records don’t just help you calculate taxes correctly. They protect you when questions come up later.

Step 2: Calculate Your Total Gross Income

Gross income is everything you brought in before you paid for anything.

That’s it. No subtracting expenses yet. No deductions. Just raw income from every source.

What counts as gross income?

Sales from your products or services are the obvious ones. But you also need to include returns and allowances (yes, even the stuff customers sent back). If you rent out part of your office space, that rental income goes here too.

Here’s where people mess up.

They think income with a 1099 vs income without a 1099 are treated differently. They’re not. The IRS doesn’t care if you got a form or not. All income is reportable.

I see this all the time. Someone does a cash job or gets paid through Venmo and figures it doesn’t count because there’s no paper trail. Wrong move.

If you earned it, you report it. Period.

When you’re ready to figure out how to calculate taxes Aggr8taxes style, this number is your starting point. Get it wrong here and everything else falls apart.

Pro tip: Keep a separate spreadsheet for income that won’t show up on official forms. Makes tax time way less stressful.

Step 3: Identify and Subtract Your Business Deductions

Here’s where you actually save money.

Deductions lower your taxable income. That means less tax owed. Simple math that most small business owners leave on the table.

The IRS has one rule for what counts as a deductible expense. It needs to be “ordinary and necessary” for your business. Ordinary means it’s common in your industry. Necessary means it helps you run your business (not that you’ll die without it).

That’s vaguer than it sounds. And that’s on purpose.

The Deductions Most Guides Get Wrong

Everyone talks about office supplies and software subscriptions. Sure, those count. But let me show you what actually moves the needle when you how to calculate taxes aggr8taxes.

Cost of Goods Sold matters if you sell physical products. This includes what you paid for inventory, materials, and direct labor. It comes off your revenue BEFORE you even calculate gross profit. Understanding the impact of Cost of Goods Sold on your revenue is crucial for gamers looking to sell physical products, and leveraging tools like Aggr8taxes can simplify the complexities of calculating expenses before determining your gross profit. For gamers venturing into the world of selling physical products, understanding the nuances of Cost of Goods Sold is essential, especially when leveraging tools like Aggr8taxes to optimize their financial strategies.

Most guides lump this in with regular expenses. Wrong. COGS gets special treatment on your return.

Operating expenses are your bread and butter deductions. Rent, utilities, internet, phone bills, software you actually use. The stuff that keeps your doors open.

Here’s what competitors won’t tell you: that gym membership? If you’re a personal trainer, it’s deductible. If you’re an accountant, it’s not. Context matters more than category.

Marketing costs are fully deductible the year you spend them. Your website, Facebook ads, business cards, that sponsored post you paid for. All of it counts.

Salaries and contractor payments include wages, benefits, and those 1099 payments to freelancers. Just make sure the compensation is reasonable for the work done.

The Home Office Deduction Everyone Screws Up

You have two options here.

The simplified method gives you $5 per square foot up to 300 square feet. That’s a maximum $1,500 deduction with zero math.

The actual expense method requires you to calculate the percentage of your home used for business, then apply that to mortgage interest, utilities, repairs, and depreciation.

Which one’s better? Depends on your situation. But here’s the thing nobody mentions: once you pick actual expenses, you can’t switch back to simplified for that property.

Vehicle expenses work the same way. Standard mileage (67 cents per mile for 2024) or actual expenses like gas, insurance, and repairs.

Most people default to mileage because it’s easier. But if you drive a newer car with high payments, actual expenses might save you more.

| Deduction Type | What Counts | What Doesn’t |

|---|---|---|

| —————- | ————- | ————– |

| COGS | Inventory, materials, direct labor | Your time, overhead |

| Operating | Rent, utilities, required software | Personal subscriptions |

| Marketing | Ads, website, business cards | Networking meals over $50 |

| Home Office | Dedicated workspace only | Bedroom you sometimes work in |

Pro Tip: Open a separate bank account and credit card for business expenses. I can’t stress this enough. Mixing personal and business transactions is how people lose legitimate deductions during audits.

The IRS doesn’t care that you “know” which charges were for business. They want clean records. Give them clean records.

Step 4: Determine Your Net Profit (or Taxable Income)

Here’s where most people mess up.

I used to think calculating taxable income was complicated. That I needed some fancy software or a degree in accounting to get it right.

I was wrong.

The formula is dead simple:

Gross Income – Total Deductions = Net Profit (Taxable Income)

That’s it. That’s the number the IRS cares about. This is what your income tax and self-employment tax get calculated from.

But here’s the mistake I made early on (and I see others make it constantly).

I’d look at my bank account and think that was my taxable income. If I brought in $100,000, I figured I owed taxes on $100,000.

WRONG.

Let’s say you earned $100,000 this year. You had $40,000 in legitimate business expenses and deductions. Your taxable income isn’t $100,000. It’s $60,000.

That’s a massive difference when tax time rolls around.

I learned this the hard way my first year freelancing. I didn’t track my expenses properly and ended up paying taxes on income I’d already spent on business costs. It hurt.

Now I know better. And when you’re figuring out how to calculate taxes aggr8taxes style, you start with this number. Your net profit. Not your gross income.

Get this step right and everything else falls into place.

Step 5: Calculate Your Income and Self-Employment Taxes

Here’s where things get real.

You’ve got your net profit from Step 4. Now you need to figure out what you actually owe the IRS.

And here’s what confuses most people. You’re not just paying one tax. You’re paying two.

Income tax and self-employment tax.

Let me break this down because the IRS doesn’t make it easy to understand.

The Self-Employment Tax Hit

This one catches new business owners off guard.

When you work for someone else, your employer pays half of your Social Security and Medicare taxes. You pay the other half through payroll deductions.

When you work for yourself? You pay both halves.

That’s 15.3% on your first $168,600 of net earnings for 2024. After that threshold, you’re looking at 2.9% for Medicare only (Social Security caps out).

I know. It stings.

But there’s a small break here. You get to deduct half of your self-employment tax when calculating your income tax. It doesn’t reduce your SE tax itself, but it does lower your taxable income for the other tax you owe. In the complex world of self-employment, understanding how to maximize your deductions—like the half deduction of your self-employment tax—can make a significant difference, and that’s where tools like Aggr8taxes come into play to simplify the process. In navigating the intricate landscape of self-employment taxes, leveraging resources like Aggr8taxes can significantly aid in maximizing your deductions and ultimately reducing your taxable income.

Think of it as the IRS acknowledging that you’re playing both employer and employee.

Your Federal Income Tax

This is the tax most people know about.

It works on a bracket system. You don’t pay one flat rate on all your income. You pay different rates as your income climbs through different brackets. The ideas here carry over into Investment Savings Aggr8taxes, which is worth reading next.

For 2024, if you’re single, the first $11,600 is taxed at 10%. The next chunk up to $47,150 is taxed at 12%. And so on.

You calculate this tax on your net profit from Step 4, minus that half of SE tax I just mentioned, minus your standard deduction.

Some folks think jumping into a higher bracket means all their income gets taxed at that higher rate. Not true. Only the dollars in that bracket get hit with that rate.

Tax Credits vs. Tax Deductions

Here’s something worth understanding.

Deductions lower your taxable income. Credits lower your actual tax bill.

If you’re in the 22% tax bracket, a $1,000 deduction saves you $220 in taxes. A $1,000 credit saves you $1,000.

Credits are better. Way better.

Common credits for business owners include the Child Tax Credit if you have kids, or the Earned Income Tax Credit if you qualify based on income.

Now, some people say you shouldn’t worry about how to calculate taxes aggr8taxes and just let software handle everything. And sure, software helps.

But if you don’t understand what’s happening behind the scenes, you can’t spot mistakes. You can’t plan ahead. You’re just hoping the numbers are right.

When you know how these calculations work, you can make smarter decisions throughout the year. Not just at tax time.

Want more strategies for managing your business finances? Check out business advice aggr8taxes for practical tips that actually work.

Step 6: Understand Estimated Taxes and Deadlines

Most small business owners don’t realize they’re supposed to pay taxes four times a year.

Not once in April like everyone else. Four times.

The IRS calls it pay-as-you-go. And if you miss it, you’ll pay penalties even if you settle up by tax day.

Here’s what nobody tells you about this system.

The IRS wants their cut as you earn it. When you had a W-2 job, your employer withheld taxes from every paycheck. Now that you’re running your own show, you’re responsible for sending those payments in yourself.

Some tax advisors say you can skip estimated payments if you’re just starting out. They figure the penalties are small enough that it’s not worth the hassle.

But that’s short-term thinking.

Those penalties add up faster than you think. I’ve seen business owners owe an extra $500 to $2,000 just because they ignored quarterly deadlines. That’s money you could’ve kept in your pocket.

When You Need to Pay

You’ve got four deadlines to remember:

- April 15 (covers January through March)

- June 15 (covers April and May)

- September 15 (covers June through August)

- January 15 of the next year (covers September through December)

Notice something weird? The quarters aren’t actually equal. The second period is only two months while the third is three. Don’t ask me why the IRS does it this way. We break this down even more in Aggr8taxes Investment Savings by Aggreg8.

If a deadline falls on a weekend or holiday, you get until the next business day.

How Much Should You Pay

This is where it gets tricky.

You need to estimate your total tax bill for the year and divide it by four. But most businesses don’t earn the same amount every quarter (especially if you’re seasonal or just starting out).

The safe harbor rule helps here. If you pay at least 90% of what you’ll owe this year or 100% of what you paid last year, you avoid penalties. For high earners making over $150,000, that jumps to 110% of last year’s tax.

Pro tip: If your income varies a lot month to month, you can use the annualized income method. It’s more paperwork but it matches your actual earnings pattern instead of forcing equal payments.

You can figure out how to calculate taxes aggr8taxes using your profit and loss statements from each quarter. Take your net profit, multiply by your tax rate (usually 25% to 35% for most small businesses when you include self-employment tax), and that’s roughly what you should send in.

What Happens If You Don’t Pay

The underpayment penalty isn’t huge but it stings.

The IRS charges interest on what you should’ve paid, calculated from each quarterly due date. Right now that rate hovers around 8% annually. So if you owed $5,000 in Q1 and didn’t pay until you filed in April of the next year, you’re looking at about $400 in penalties.

That’s $400 you just handed over for no reason.

The thing most competitors won’t tell you? You can adjust your estimated payments throughout the year. Had a slow Q2? Pay less in June. Landed a huge client in Q3? Bump up your September payment.

The IRS doesn’t care if your payments are uneven as long as you hit that safe harbor threshold by year end.

One more thing. Some states have their own estimated tax requirements with different deadlines. California, New York, and Illinois are particularly strict about this. Check your state’s rules separately because the IRS won’t remind you about state obligations. To navigate the complex landscape of state tax obligations, especially in stringent states like California, New York, and Illinois, gamers should consider utilizing Aggr8taxes Savings Tips to ensure they remain compliant and avoid any unexpected penalties. To ensure you’re fully prepared for any state-specific tax obligations, be sure to explore the Aggr8taxes Savings Tips that can help you manage your finances effectively, especially in states with stringent requirements like California, New York, and Illinois.

Set calendar reminders for these dates right now. Missing one deadline starts a domino effect that’s hard to recover from.

From Calculation to Confidence

You now have a complete process for calculating your small business taxes.

I know the numbers can feel overwhelming. But when you break it down into these steps, the anxiety disappears. So does the risk of making costly mistakes.

This structured approach does three things for you. It stops you from overpaying. It helps you claim every deduction you’ve earned. And it keeps you compliant with the IRS.

Here’s what to do next: Start organizing your finances today using this guide. Get your receipts in order and begin tracking your expenses if you haven’t already.

For complex situations (and some tax scenarios get messy fast), consider working with a tax professional. They’ll catch things you might miss and can save you more than they cost.

how to calculate taxes aggr8taxes gives you the framework. Now it’s up to you to put it into action.

The difference between guessing and knowing your tax situation is worth the effort. You’ll sleep better and keep more of what you earn.

Thadrian Xenvale is the kind of writer who genuinely cannot publish something without checking it twice. Maybe three times. They came to tax tips and strategies through years of hands-on work rather than theory, which means the things they writes about — Tax Tips and Strategies, Tax Deductions and Credits, Financial Planning for Taxes, among other areas — are things they has actually tested, questioned, and revised opinions on more than once.

That shows in the work. Thadrian's pieces tend to go a level deeper than most. Not in a way that becomes unreadable, but in a way that makes you realize you'd been missing something important. They has a habit of finding the detail that everybody else glosses over and making it the center of the story — which sounds simple, but takes a rare combination of curiosity and patience to pull off consistently. The writing never feels rushed. It feels like someone who sat with the subject long enough to actually understand it.

Outside of specific topics, what Thadrian cares about most is whether the reader walks away with something useful. Not impressed. Not entertained. Useful. That's a harder bar to clear than it sounds, and they clears it more often than not — which is why readers tend to remember Thadrian's articles long after they've forgotten the headline.

Thadrian Xenvale is the kind of writer who genuinely cannot publish something without checking it twice. Maybe three times. They came to tax tips and strategies through years of hands-on work rather than theory, which means the things they writes about — Tax Tips and Strategies, Tax Deductions and Credits, Financial Planning for Taxes, among other areas — are things they has actually tested, questioned, and revised opinions on more than once.

That shows in the work. Thadrian's pieces tend to go a level deeper than most. Not in a way that becomes unreadable, but in a way that makes you realize you'd been missing something important. They has a habit of finding the detail that everybody else glosses over and making it the center of the story — which sounds simple, but takes a rare combination of curiosity and patience to pull off consistently. The writing never feels rushed. It feels like someone who sat with the subject long enough to actually understand it.

Outside of specific topics, what Thadrian cares about most is whether the reader walks away with something useful. Not impressed. Not entertained. Useful. That's a harder bar to clear than it sounds, and they clears it more often than not — which is why readers tend to remember Thadrian's articles long after they've forgotten the headline.